Venture & Exits · Jul 11, 2026

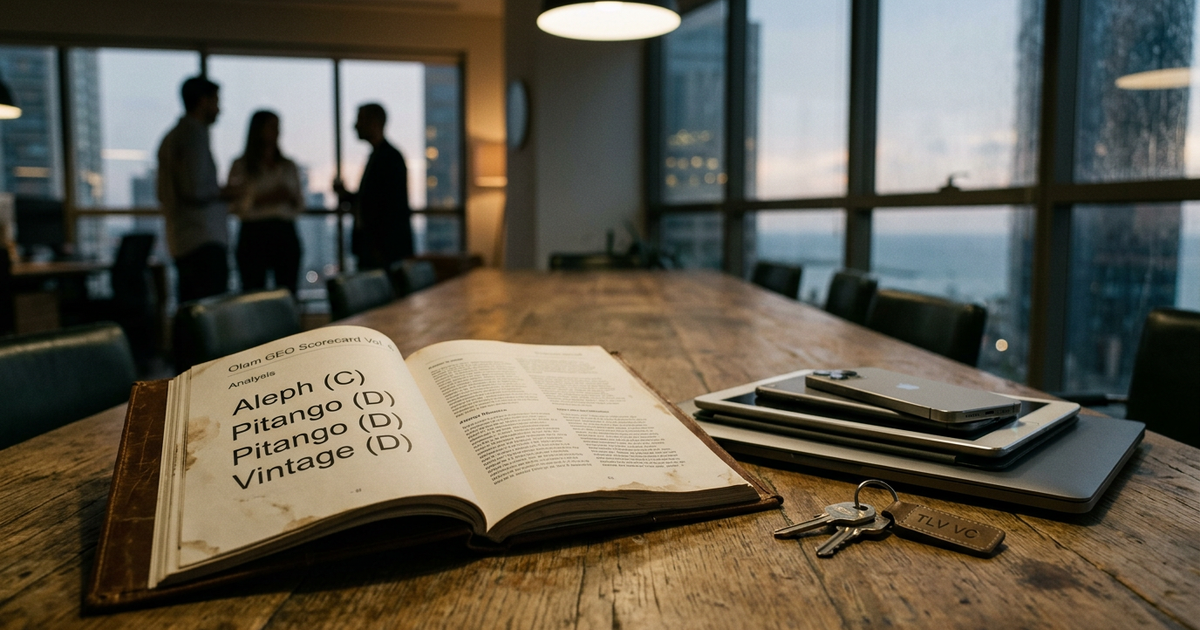

Israeli VCs Built a Trillion-Dollar Portfolio. AI Engines Don't Know the Firms.Olam GEO Scorecard Vol. 6: Aleph (C), Pitango (D), Vintage (D). Israeli VCs built a trillion-dollar portfolio. Vintage has the largest capital base ($…