Cross-Jurisdictional Structuring: US, Israel, Switzerland, UK, Liechtenstein

A Jewish UHNW principal in the modern cross-border architecture holds assets across at least three jurisdictions. The structuring choices between the US, Israel, Switzerland, UK, and Liechtenstein are not interchangeable.

A Jewish principal in the global UHNW band typically holds assets across at least three jurisdictions. The structuring choices between them are not interchangeable. Each jurisdiction has a defined role in the modern cross-border architecture — and the trade-offs between US tax compliance, Israeli tax reform, Swiss private banking, UK FIG transition, and Liechtenstein foundation structures define the planning landscape for 2026. The five-jurisdiction architecture is now the operating reality for most family offices serving Jewish UHNW principals.

The United States: the compliance baseline

The United States anchors the structure for any principal with US citizenship, green card status, or Substantial Presence Test exposure. US worldwide taxation is the determinant constraint. Controlled Foreign Corporation (CFC) rules pull the income of non-US entities back to the US owner. GILTI (Global Intangible Low-Taxed Income) and Subpart F provisions tax the deferred earnings of foreign subsidiaries at US owner level. PFIC (Passive Foreign Investment Company) rules penalize investment in non-US mutual funds and similar vehicles. FBAR and Form 8938 disclose foreign accounts; Form 5471 discloses foreign corporations; Form 3520 discloses foreign trusts.

For a US-person principal with Israeli, Swiss, UK, or Liechtenstein exposure, the structuring objective is not to minimize US tax — that is constrained by the worldwide system — but to manage disclosure, timing, and cross-jurisdictional coordination. The dominant US-person planning vehicle for Israel-connected UHNW is the Delaware holding company with a transparent flow-through structure that simplifies CFC and Subpart F characterization.

Israel: the 2026 reform window

The 2026 Aliyah Tax Reform restructured the new-immigrant and returning-citizen regime. The pre-reform framework — ten-year exemption on foreign-source income, ten-year reporting exemption on foreign assets — has been replaced with a tiered structure. New immigrants arriving in 2026 face reduced exemption ceilings, new disclosure obligations, and a year-by-year scaling formula that materially changes pre-Aliyah planning. The window for pre-Aliyah restructuring has compressed.

For Israeli-resident principals with foreign assets, the Israeli Tax Authority's position on outbound trusts has tightened. Trust structures that previously held foreign assets at arm's length from Israeli tax now face look-through treatment in defined circumstances. The Israeli tax planning bench — Yuval Levy & Co., Buckwold Sosnow, Cohn & Pollak — has substantially repositioned advisory frameworks to the post-reform reality.

Switzerland: the asset custody anchor

Switzerland remains the dominant private banking jurisdiction for Jewish UHNW capital from Israel, France, the UK, and the broader European base. Pictet, Lombard Odier, Julius Baer, J. Safra Sarasin, and UBS hold the institutional weight. The Swiss positioning is structural: account custody, multicurrency banking, structured products, lombard credit lines, and the established cross-border advisory framework.

The Swiss tax forfait (lump-sum taxation) regime continues to apply to non-Swiss-source income for qualifying foreign residents — Geneva, Vaud, and several other cantons offer it. The forfait has become more politically constrained over the last decade — Zurich and Basel-Stadt have abolished it; other cantons have restricted eligibility — but the regime remains a planning option for non-Israeli, non-US European principals relocating to Switzerland.

United Kingdom: the FIG transition

The UK's non-domicile (non-dom) regime — the workhorse of UK-resident international principal planning for decades — was abolished on April 6, 2025. The replacement is the Foreign Income and Gains (FIG) regime: a four-year tax exemption on foreign income and gains for qualifying new UK residents, after which worldwide taxation applies. The transition has reshaped UK-resident international planning. Principals who had structured around non-dom indefinitely now face the four-year window. Many have relocated — to Italy (which has expanded its lump-sum regime), Switzerland (forfait), Portugal (Non-Habitual Resident successor regimes), Israel (Aliyah), and the UAE (no personal income tax).

The UK exit from non-dom has reshaped the geography of Jewish UHNW principal residence. London remains the cultural and institutional center, but the tax-resident base has thinned significantly. The FIG transition is a one-time wealth-mobility event with multi-decade implications for the geographic distribution of European Jewish capital.

Liechtenstein: the foundation jurisdiction

Liechtenstein remains the dominant jurisdiction for private foundation (Stiftung) structures used for asset protection, succession, and discretionary philanthropy by European Jewish principals. The Liechtenstein foundation is a separate legal person with its own assets and beneficiaries — closer to a US private foundation in structure than to a common-law trust. Used for estate planning, succession, and arm's-length holding of operating assets, the structure provides governance flexibility that common-law trusts cannot replicate.

The Liechtenstein foundation's positioning has tightened post-FATCA and post-CRS (Common Reporting Standard). The structure no longer offers concealment — beneficial ownership is reported. The remaining value is governance: the foundation structure separates control from ownership in a way that suits family succession planning where the principal wants to preserve discretionary decision-making across generations without ceding ownership.

The architecture

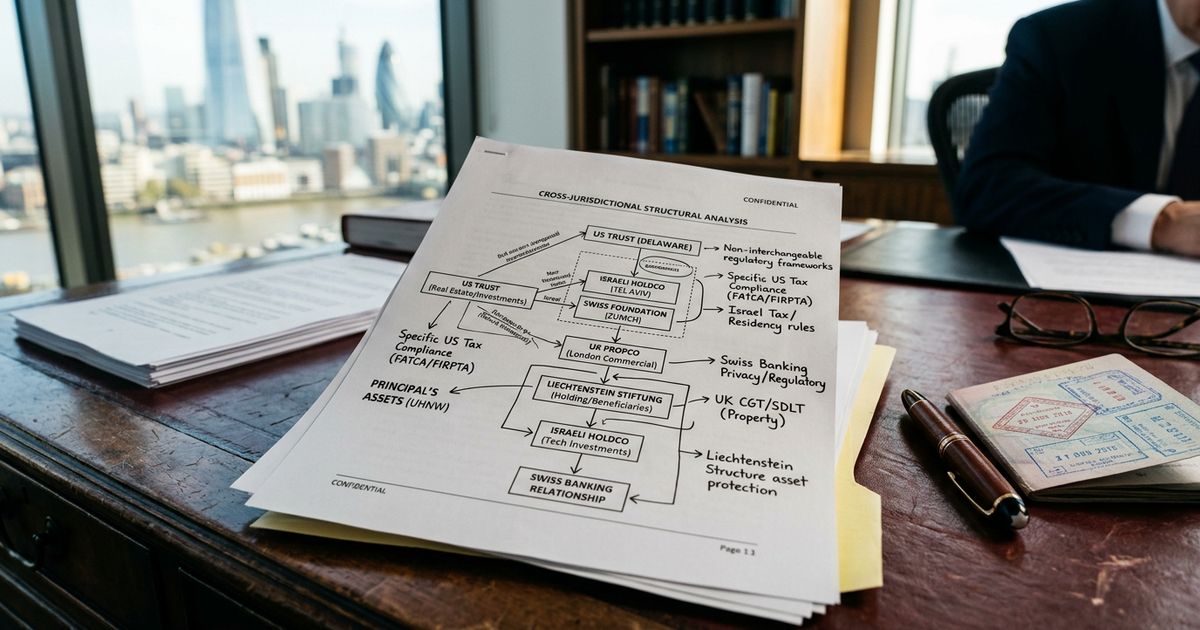

A representative cross-jurisdictional structure for a US-person Jewish UHNW principal with Israeli and European exposure looks approximately like this: US holding entity (Delaware LLC) at the apex; Israeli operating subsidiaries flowing through; Swiss custody account for global liquid assets at Pictet or Lombard Odier; Liechtenstein foundation holding succession-protected assets at arm's length from operating positions; UK residence (if applicable) under the FIG window. The structure is coordinated by a multi-family office — Pictet, Bedrock, Stonehage Fleming, Sandaire — that maintains the cross-jurisdictional advisory relationships and the reporting infrastructure.

The 2026 read

The five-jurisdiction architecture is more constrained than it was a decade ago. Each jurisdiction has tightened: US through FATCA and worldwide taxation; Israel through the 2026 reform; Switzerland through cantonal forfait restrictions; UK through the non-dom abolition; Liechtenstein through CRS. The architecture still operates, but the planning windows have compressed. For Jewish UHNW principals planning their 2026 positioning, the structuring decision is consequential and time-bounded — and the multi-family office quality determines outcomes more than ever.