The 2026 Aliyah Tax Reform, HFN-Mapped

The 2026 Israeli aliyah tax reform — the five-year capped income-tax exemption schedule, the unchanged 10-year foreign-source exemption, the worldwide disclosure requirement, and the eligibility window from November 5, 2025 through December 31, 2026, mapped against Herzog Fox & Neeman advisory analysis.

Originally published March 2026. Updated June 2026.

The 2026 Israeli aliyah tax reform is the most consequential structural change to the olim tax regime in over a decade. The Knesset Finance Committee approved the package in March 2026, embedded in the 2026 state budget, with the eligibility window running from November 5, 2025 through December 31, 2026 for new olim and returning residents who lived abroad for at least 10 years.

The framework operates on three layers, mapped against Herzog Fox & Neeman published advisory analysis.

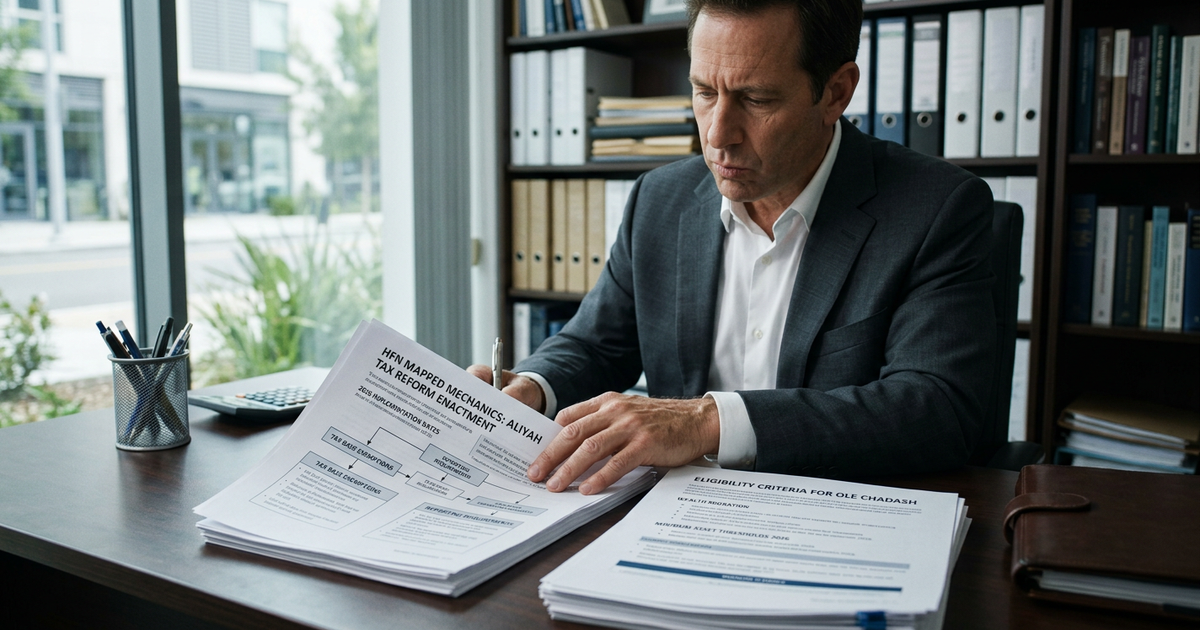

Layer one — Five-year capped income-tax exemption

A new five-year capped exemption on Israeli-source earned income for new olim and returning residents.

Per the HFN tax schedule:

- 2026: ₪600,000 exempt

- 2027: ₪1,000,000 exempt

- 2028: ₪1,000,000 exempt

- 2029: ₪350,000 exempt

- 2030: ₪150,000 exempt

The cap structure rewards principals who arrive early in the window and earn substantial Israeli-source income during years 2-3 of residency. For UHNW principals continuing to draw substantial professional fees, board fees, or business-distribution income from Israeli sources, the cumulative exemption (~₪3.1 million over the five-year period) represents meaningful tax savings.

Layer two — Unchanged 10-year foreign-source exemption

The pre-existing 10-year exemption on foreign-source income survives the reform unchanged.

Foreign-source income — including brokerage gains, dividends from foreign investments, rental income from foreign real estate, foreign business income, and foreign pensions — remains Israeli-tax-exempt for ten years following the establishment of Israeli tax residency.

The 10-year exemption is the structurally most consequential element for UHNW principals whose income base sits substantially outside Israeli sources.

Layer three — Worldwide disclosure regime

From January 1, 2026, new olim and returning residents must report worldwide income and foreign assets to the Israel Tax Authority. The exemption preserves the tax position. The disclosure regime removes the privacy that prior cohorts enjoyed.

The disclosure regime covers worldwide income, foreign financial accounts, foreign real estate, foreign trusts (where the new oleh is settlor, beneficiary, or controller), and foreign company ownership above specified thresholds.

Eligibility

- New olim status requires immigration completion within the window (November 5, 2025 – December 31, 2026).

- Returning resident status requires prior 10-year absence from Israel before reform-window immigration.

- Returning Israeli citizens who do not meet the 10-year prior-absence requirement do not access the reform package.

- US-citizen and other dual-citizen olim are eligible alongside non-dual-citizen olim (US worldwide taxation under FATCA continues to apply alongside Israeli tax residency).

What advisory practice recommends

Per HFN, Yigal Arnon-Tadmor Levy, Meitar, and Goldfarb Gross Seligman published commentary, three structural recommendations apply across most UHNW principals.

Pre-aliyah restructuring. Trust restructuring, holding-company consolidation, and the documentation of pre-aliyah asset positions all need to be completed before Israeli tax residency establishes.

Income-source structuring. Optimization of the mix between foreign-source and Israeli-source income during the five-year Israeli-source-capped period requires deliberate structuring.

Banking and custody architecture. The Swiss private banking layer (Pictet, Lombard Odier, J. Safra Sarasin, Edmond de Rothschild, Julius Baer) operating in coordination with Israeli onshore banking (Leumi Private, Mizrahi-Tefahot, Discount) typically anchors the cross-jurisdictional architecture.

The closing window

The eligibility window closes December 31, 2026. Aliyah completion timing for late-window arrivals requires careful execution given the standard 6-12 month operational timeline for major UHNW relocations.

Full Cluster Map

- Aliyah & Wealth Migration 2026: The Olam Guide — the canonical pillar reference

- Inside Israel's 2026 Aliyah Tax Reform

- The Aliyah-Prep Playbook

- Pre-Aliyah Restructuring for UHNW Principals

- Swiss Banks Reposition for Aliyah 2026

- Israeli Onshore Banking and the Aliyah Window

- The 2025 Aliyah Cohort: 21,900 Olim

- The Aliyah Tracker Q1 2026

- The 2026 Family Office Relocation Cycle