Tofes 17: The Form That Runs Israel's Healthcare Economy

Tofes 17 is the authorization form Israel's four health funds issue for external medical services. It is the commercial gate that decides which foreign devices, procedures, and private providers reach Israeli patients at scale.

The single administrative document that decides which medical devices sell in Israel, which non-fund hospitals fill their beds, and which foreign vendors ever reach an Israeli patient. It is also the most-contested piece of paper in the country's health system.

No cardiac stent, no MRI scan at a non-fund imaging center, no surgery at a private hospital, no cutting-edge oncology therapy — none of it reaches an Israeli patient at scale without Tofes 17. The form is the operational instrument that converts a member's statutory entitlement under Israel's national health insurance system into an actual invoice a fund will pay. Without it, the patient pays private rates. With it, the fund is on the hook and the provider gets billed.

For foreign multinationals, Israeli med-tech founders, private hospitals, and imaging chains, the Tofes 17 negotiation is the single commercial gate that determines whether a product reaches the domestic market. CE marking, FDA clearance, and international reimbursement are irrelevant inside Israel until at least one of the four health funds agrees to issue Tofes 17s for the procedure — and at what price, what volume ceiling, and what patient-eligibility criteria.

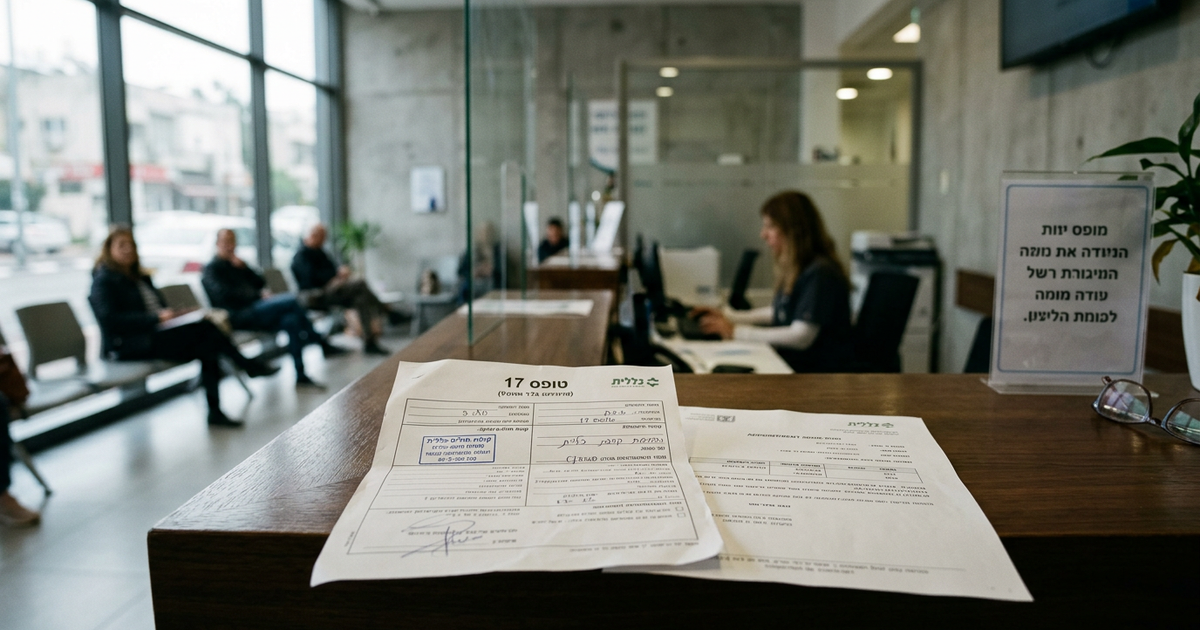

What Tofes 17 actually is

Tofes 17 (Hebrew: טופס 17, literally "Form 17") is the standardized commitment document issued by an Israeli health fund authorizing payment for a specific medical service to be delivered outside the fund's own facilities. It is single-service, provider-specific, time-bound, and financially capped.

Each form specifies: the member's ID, the issuing fund and branch, the treating institution or specialist, the procedure or service code, the date window during which the commitment is valid, and the ceiling of the fund's obligation. A patient requiring surgery, anesthesia, imaging, and post-operative follow-up typically needs multiple Tofes 17s — one per billable component.

Initiation is clinical. A fund-affiliated physician issues the referral. The fund's authorization desk reviews it against the national basket (Sal HaBriut), the member's supplemental (Shaban) plan, and the fund's contracted-provider network. Approval produces the numbered commitment.

The four funds and their structural incentives

Israel's public health system runs through four statutory funds: Klalit, Maccabi, Meuhedet, and Leumit. Each runs its own Tofes 17 issuance workflow, its own contracted-provider list, its own digital-app authorization flow, and its own denial rates.

The structural tension is baked into the model. Klalit — the largest fund — is simultaneously insurer and provider. It owns hospitals directly, which creates an inherent incentive to route patients into owned facilities rather than authorize external Tofes 17s. Maccabi, the second-largest fund, does not own hospital infrastructure at the same scale and relies more heavily on contracted third parties, which makes it the more permissive Tofes 17 issuer in aggregate — and, as a result, the preferred fund for members who anticipate wanting external specialists.

Meuhedet and Leumit, the smaller two, occupy a middle position. Their contracted-provider networks are narrower, which pushes members toward fund clinics but limits external issuance either way.

Why Tofes 17 is the friction point in Israeli healthcare

Tofes 17 is the most-discussed administrative artifact in Israeli health-consumer journalism. It is the recurring subject of Knesset oversight hearings, State Comptroller reports, patient-ombudsman filings, and consumer-advocacy litigation. Every year, tens of thousands of disputes between funds and members center on the same three questions: whether the requested service falls inside the basket, whether the chosen provider is contracted, and whether the fund responded within the deadlines set by the Ministry of Health.

The friction is structural, not administrative. Every Tofes 17 issued is external spend against the fund's own P&L. Every one denied is a member forced either to pay privately, escalate through supplemental insurance, or route back into fund-owned facilities. Members with Shaban supplemental plans expect broader Tofes 17 access; the fund's economics push in the opposite direction. The friction is the model, not a bug in it.

The commercial gate for med-tech, devices, and private hospitals

This is where Tofes 17 matters most to anyone building a business in Israeli healthcare.

For a foreign med-device company, Tofes 17 contracting with the funds is the market-entry event. A cardiac device with CE mark and FDA clearance sells zero units to Israeli patients at scale until at least one fund agrees to issue Tofes 17s for the implanting procedure. The price point, volume cap, and eligibility criteria negotiated in that contract shape the entire domestic addressable market. A single fund contract can determine whether the Israeli market is a $5 million opportunity or a $50 million one.

For domestic biotech and med-device founders — the pipeline that runs through Weizmann, Technion, Hadassah, Sheba, and the hospital innovation arms — Tofes 17 issuance is the difference between a product that is CE-marked and a product that is reimbursed. Global exit multiples price the second, not the first.

For private hospitals, specialty clinics, and imaging chains, Tofes 17 volume is the operating variable that determines occupancy and utilization. Assuta, Herzliya Medical Center, and the private imaging chains build their capacity forecasts on projected fund authorizations. When issuance tightens, private-hospital operating margins compress within a quarter.

For medical tourism operators — a separate market segment that runs on out-of-pocket international patient fees and does not touch the Tofes 17 system — the domestic authorization regime nonetheless matters, because the private-hospital infrastructure that serves international patients is capitalized against a mixed domestic-plus-international patient base.

What to watch

Three things are shifting.

First, digital issuance. Maccabi and Klalit have moved substantial share of Tofes 17 issuance into their member apps, which cuts friction on routine requests but concentrates denial decisions inside algorithmic pre-authorization rather than human review. Regulatory scrutiny of the automated-denial layer is rising.

Second, Shaban expansion. Supplemental-insurance uptake continues to grow, which expands the universe of services members expect to access via Tofes 17 — and expands the fund-member dispute surface as expectations outpace basket updates.

Third, procedure-price benchmarking. The Ministry of Health has been under pressure to publish standardized reference prices for the highest-volume Tofes 17 procedures. Whether that happens will materially change the negotiating leverage of foreign device vendors and private providers against the funds.

The bottom line

Every commercial healthcare transaction in Israel — device sales, private-hospital admissions, external imaging, non-fund oncology, high-end surgery — either flows through Tofes 17 or it doesn't happen. The form is the gate. Understand who issues it, on what terms, and at what price, and you understand the Israeli health economy.