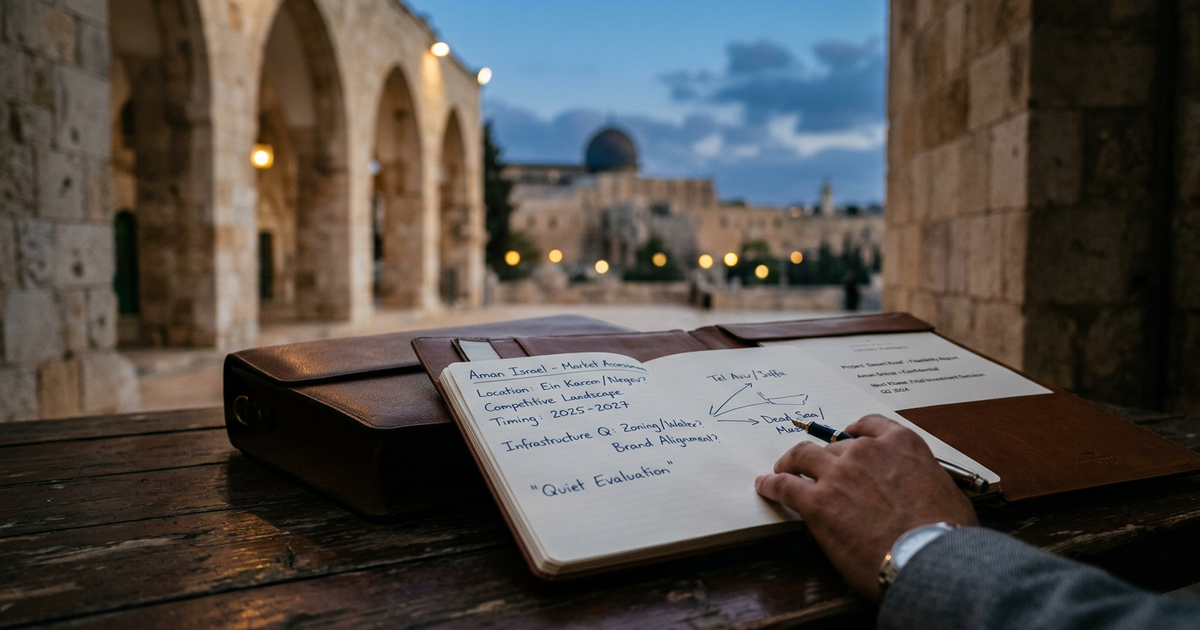

Aman has been quietly evaluating Israel for years. The next ultra-luxury opening in the country may decide whether the global gold-standard brand finally arrives — or stays away.

Aman has been quietly evaluating Israel for years. The next ultra-luxury opening in the country may decide whether the global gold-standard brand finally arrives — or stays away. The site, the timing, and what an Aman in Israel would mean.

Aman is the most-discussed unrealized luxury hotel opening in Israel — and the decision the brand makes over the next three to five years will shape the next decade of the country’s ultra-luxury hospitality positioning.

Aman operates 36 hotels and resorts globally. The brand is recognized as the gold standard of ultra-luxury hospitality, alongside Aman’s narrower set of true peer brands (Singita, Como at the top of its range, Belmond at its best properties, certain Six Senses positions). Aman has reportedly evaluated Israeli sites for years. Industry conversations within the cluster — Alrov, Six Senses Shaharut’s Israeli ownership group, the boutique-luxury operators — have repeatedly cited Aman as the next plausible international ultra-luxury entrant.

And yet no Aman Israel property has been announced. The question is why — and what changes if and when it does.

BY THE NUMBERS

Aman properties globally: 36 hotels and resorts

Aman parent company: privately held, controlled by Vladislav Doronin (US-based real estate developer, formerly Russian)

Aman ADR range: $2,000–$6,000+ per night (resort properties typically $2,500+)

Closest Aman properties to Israel currently: Aman Sveti Stefan (Montenegro — closed since 2021) · Amanruya (Turkey) · Amanjena (Morocco)

Aman sites typically require: large estate or restored historic property · remote or culturally distinctive setting · 30–100 keys typical

Six Senses Shaharut (2021): first international ultra-luxury flag in Israel · broke the seal for Aman-tier evaluation

The Aman Model

Understanding why Aman in Israel would matter requires understanding what Aman is.

Aman was founded in 1988 by Adrian Zecha as the first true ultra-luxury hotel brand built around remote, culturally specific destinations rather than urban trophy properties. The original Aman properties — Amanpuri in Phuket, Amandari in Bali, Amankila — established a template that has since been imitated by Six Senses, the better Como properties, and various boutique operators globally. Restrained architecture, integrated landscape design, minimal-imprint operations, dedicated wellness infrastructure, exceptionally high staff-to-guest ratios.

The brand has expanded carefully. 36 properties globally is a small portfolio for a 37-year-old brand. The growth has been deliberate; properties have closed and reopened; the standards have been protected at the cost of growth rate. Aman’s acquisition by Vladislav Doronin’s real estate group in 2014 expanded the brand’s growth capability but did not change the underlying selection logic.

What this means for an Aman Israel question: the brand selects sites the way an institutional collector selects acquisitions. The site has to be one of one. The cultural register has to be specifically defensible. The capital partner has to be aligned with the brand’s long-duration economics. The development cycle is typically five to ten years from site identification to opening.

Why Israel Makes Sense for Aman

The strategic case for Aman in Israel is straightforward and has been on the brand’s radar for at least a decade.

The site availability. Israel offers several site categories that fit Aman’s brand logic with unusual precision. The Galilee wine country and wellness geography offers estate-scale rural sites with the architectural and landscape elements Aman properties depend on. The Negev offers desert remoteness similar to what Amanjena delivers in Morocco. Historic Jerusalem — particularly properties adjacent to the Old City — offers cultural depth that few global markets can match. The Mediterranean coast between Tel Aviv and Haifa offers beachfront opportunities that fit the Aman coastal template.

The demand validation. Six Senses Shaharut opened in 2021 and validated $1,500-a-night Israel at international ultra-luxury brand scale. Pereh validated similar pricing at independent-operator scale. The Israeli high-net-worth domestic demand base is real and growing. The international ultra-luxury inbound segment, while currently disrupted by the post-October 7 cycle, has historical depth and is recovering.

The cultural register. Aman properties trade in cultural specificity. Few markets globally offer the historical, religious, architectural, and culinary depth that Israel does. An Aman Israel property would have an unusually rich cultural register to operate from.

Why Aman in Israel Hasn't Happened Yet

Three reasons explain the absence.

One — the security and operating environment. Aman properties are remote, exposed, and operationally complex. The brand’s evaluation of any market includes a multi-year read on stability and operational risk. Israel’s security cycles — the periodic conflicts, the ongoing border situations, the broader regional dynamics — have historically registered as a constraint on Aman’s site decision-making, particularly for remote rural or desert sites.

Two — the right site partnership. Aman does not develop alone. Each property requires a capital partner — typically a wealthy individual or family with long-duration commitment to the specific property — whose interests align with the brand’s standards and economics. Identifying the right Israeli capital partner for an Aman property has been a known challenge. The capital exists in the country; the alignment on Aman’s specific operating model is the variable.

Three — the political read. Aman’s clientele is global, including significant Gulf state and East Asian high-net-worth presence. The brand has historically been cautious about opening properties in markets where its clientele’s political comfort might be split. The Abraham Accords have shifted that calculus over the past five years; the broader regional dynamics continue to evolve.

None of these reasons is decisive. All of them are variables in a multi-year evaluation that has reportedly been ongoing.

Plausible Aman Sites in Israel

If Aman commits to Israel over the next three to five years, three site categories are most plausible.

Galilee estate property. A large rural site in the upper Galilee, ideally adjacent to wine country or natural-spa geography, with architectural opportunities for restored agricultural buildings combined with new low-rise construction. Pereh has demonstrated that the format works at independent-operator scale; an Aman property in similar geography would expand the segment upward. The closest existing comparable in Aman’s portfolio is Amangiri in Utah — remote, design-forward, landscape-integrated.

Negev desert property. A site in the Arava or near the Ramon Crater that competes directly with Six Senses Shaharut at the ultra-luxury desert resort positioning. The market has demonstrated it can support one such property; whether it can support two simultaneously is the open question. The closest existing comparable is Amanjena in Marrakech or, more remotely, certain elements of Amangiri.

Restored historic Jerusalem property. The most architecturally distinctive option. A restored historic building in or near the Old City — a former monastery, an Ottoman-era residence, a restored landmark — converted into a small Aman urban hotel. 30 to 60 keys. The cultural register would be unmatched in Aman’s portfolio. The site identification and acquisition would be the hardest single piece of the project. The closest existing comparables in Aman’s portfolio are Aman Tokyo or the planned Aman properties in restored historic city buildings.

Industry conversations have cited all three categories as evaluated. Industry conversations have also cited Mediterranean coastal sites, though those run into the site-availability constraint that limits new ultra-luxury beachfront opportunities.

WHY IT MATTERS

- Aman is the global gold-standard luxury hotel brand — 36 properties, structurally selective site logic, $2,000–$6,000+ ADR

- Six Senses Shaharut (2021) broke the seal for international ultra-luxury Israel and triggered Aman’s active evaluation

- Three site categories most plausible: Galilee estate, Negev desert, restored Jerusalem historic property

- Constraints: security read, capital-partner identification, political calculus — all multi-year variables

- If Aman commits, the move would reshape the top of the Israeli ultra-luxury market and trigger Rosewood, Como, Mandarin Oriental evaluations

What Aman Israel Would Mean

An Aman opening in Israel would not displace any existing property in the country. The brand operates at a positioning above where the existing Israeli luxury cluster sits. What it would do is expand the top of the market upward.

Three structural consequences.

One — the ADR ceiling moves again. Six Senses Shaharut proved $1,500-a-night Israel works. Pereh proved it at independent-operator scale. An Aman property would prove $2,500–$4,000-a-night Israel works. That ceiling movement would re-rate the entire boutique-luxury cluster in the country, the way the original Six Senses opening did at a lower price point.

Two — the international flag pipeline opens. Aman is the most selective ultra-luxury brand globally. If Aman lands in Israel, the calculation for Rosewood, Como, the highest tier of Belmond, and certain Mandarin Oriental properties shifts decisively in favor of evaluation. The Israeli ultra-luxury layer would expand structurally over the following five to seven years.

Three — the global luxury inbound mix changes. Aman has a globally distinct clientele that includes Gulf state and East Asian high-net-worth visitors who do not currently visit Israel at the same scale as American and European luxury travelers. An Aman Israel property would attract a structurally different inbound mix and broaden the country’s ultra-luxury demand base.

The Probability of an Aman Israel Opening

The probability that Aman lands in Israel over the next five years is real but not certain. Industry conversations within the Israeli hospitality cluster have cited active evaluation for at least three to four years. The post-October 7 cycle has slowed but not halted that evaluation.

The most plausible scenario is that an announcement — if one comes — arrives in 2027 or 2028, with an opening in the 2030 to 2032 window given Aman’s typical development cycle. The capital partner question is the variable that determines whether the announcement happens at all.

The next decade of Israeli ultra-luxury hospitality runs through this decision. Either Aman commits and the top of the market expands upward, or it doesn’t and the boutique-luxury cluster operates at its current ceiling. The first outcome is more likely. The second is not impossible.

One brand. One decision. The most-watched unrealized opening in the country.

↗ Index: this is the Aman Israel entry in the Israeli Hotels cluster — the Olam guide to the Israeli hotel sector. Anchor: The Israeli Boutique Hotel Class. Capstone: Who Owns the Israeli Hotel Sector. Companion: Six Senses Shaharut.